Most people know when they’re overpaying the seller as they buy a house. Most people don’t know how how much they’re going to end up paying the bank if they only pay the minimum mortgage every month…

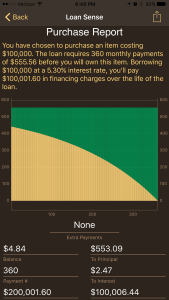

How much is the house worth?

$92,000

What price was agreed on for the house?

$100,000

How much is the buyer paying for the house?

$200,002

Can that be right? Yes, sadly it is.

At 5.3042% APR, the interest costs more than the principal over a 30 year fixed rate loan.

There is a lot of money to be made in financing charges. Before getting into any new financing situation, consider seriously if you can afford the true value of the item that’s being purchased… and if financing is necessary, what that will cost over the years.

Some items are typically financed for longer than other items. Here are some typical timeframes for buying different items:

Loans typically secured by the purchased item:

Houses: 180 or 360 months. Houses have relatively stable values and long lives with proper care – taking 30 years to pay for one isn’t strange.

Cars (Purchase): 48 to 72 months. Watch out – the manufacturer’s warranty ends before the financing does so buyers can be left with some extra major expenses at the end.

Cars (Lease): 24 to 36 months. Some cars don’t “lease well” and others are fantastic deals. These vary by manufacturer and even by model.

Boats: 120 to 180 months. Boats hold their value much better than cars do, and they aren’t being manufactured by the millions every year. Have some extra cash handy – they’re expensive to fix!

Airplanes: 120 to 240 months. Airplanes hold their value exceptionally well over the years if they are maintained properly. Maintaining an airplane is expensive, and flying one is even more expensive – the faster they can go, the more they cost.

Business: 3 to 300 months. These vary wildly depending on the lender, amount, and specific purpose. Be prepared for the bank to thoroughly examine the businesses financials.

Loans protected from bankruptcy discharge:

Education: 240 to 300 months. Depending on how much is borrowed, federal vs private, the individual income, and deferments. Loans that aren’t satisfied after 20-25 years may be eligible for forgiveness.

Unsecured debt:

Credit cards: Lifetime. Many Americans live in constant credit card debt throughout their lives. Paying the minimums will allow the balances to grow. Use our app to figure out your own payback plan on a timeline you can afford!

Borrowing an amount of money obligates the buyer to repay the money. The buyer is usually NOT obligated to make a certain number of payments. The loan agreement specifies the exact obligations for that specific loan – refer to that document when making decisions.

The monthly payment is actually a minimum amount which is due each month while there is still principal owed on the loan.

Paying the minimum every month will result in making all the minimum monthly payments for the specified number of months. Paying the minimum and going the distance is the most expensive course of action for the buyer, and sometimes there are other options. Again – review the loan agreement to confirm all options.

Usually there are two ways to make extra payments, and every extra payment should specify for the lender exactly how the payment should be allocated. The two ways are:

Allocate the amount as an Early Payment

Allocate the amount to Principal

Sending in an early payment allows the buyer to skip a payment later. When the payment is finally applied, it will satisfy the same interest and principal that the payment would have if it was submitted immediately before being applied. This is good for buyers who have sporadic income and want to build a safety net into their financial plan.

Sending in an extra payment allocated to Principal will immediately reduce the principal of the loan. That amount of principal will stop earning interest for the lender. The buyer must still make the minimum payment amount the next month, but the extra amount which was submitted (and the interest) can satisfy the loan earlier and cost less overall.

Here’s an example which saves $100k by sending extra principal payments monthly – that’s college for 2 kids!

A 30-year fixed-rate loan for 2,000 @ 4.5% APR can save 100k and end 8 years early by paying an extra 372/month.

Extra payments can be very powerful. A number of payments listed in the loan documents is NOT the simple end of a story.

A Down Payment is additional money you bring to the deal, and pay before the normal monthly payments start.

Sometimes lenders avoid risk by requiring that you put in money at the beginning of a deal. Instead of the lender having all the initial risk, a down payment gives the borrower some immediate equity and an incentive to keep paying.

A down payment also reduces the effective amount being borrowed, which creates a more affordable monthly payment.

The initial down-payment may help avoid a negative equity situation during the life of the loan.

You have Equity when the current resale value of a purchased item is more than the remaining borrowed balance. The item is worth more than is owed – to get out of the loan: sell the item and pay off the loan, then keep the extra money. This is a good position to be in.

You have Negative Equity when the remaining balance owed on a purchased item is more than the current resale value. More is owed on the item than the item is currently worth – to get out of the loan: sell the item and pay down the loan, add more money to complete the loan payoff.

Using a significant down-payment can create equity with large purchases, and provide some protection against negative equity over time. Lenders sometimes insist on a down-payment.

Borrowing money to purchase a car can create a negative equity situation, especially when there’s no down-payment, a higher interest rate, and financed over a longer period of time. Gap insurance is sometimes available as part of an auto-insurance policy to cover the difference in value if the car gets totaled while in a negative equity situation.

The borrower is legally responsible for repaying an entire loan, even if the financed item quickly becomes worthless.

Sales-people get paid to sell things – cars, televisions, real-estate, and everything in-between.

They’re incentivized to sell more than their coworkers. Bending a rule can give them an edge over their coworkers, but only until their coworkers begin bending that rule too and everyone is doing it. Then someone goes and bends that rule further, and the cycle continues until management actually enforces a limit.

You’re depending on the management of a corporation to protect your integrity and purchasing experience. Finding a good deal may not be easy.

Determining the fair market-value at some projected point in the future can be very difficult to do accurately. Companies that lease cars hire mathematicians to provide the most accurate answers, but there are reasons they might want that number to be higher, or lower.

A higher final value can be good for everyone – consumers pay less during the lease, the dealership gets to control the price again when the lease is over, and the brand gets to highlight the retained value in their products while driving up the prices of used goods – which also support even-higher rates for new goods.

A lower number is great for the dealerships because the user overpays during the lease. Undervaluing the car is bad for the buyer who pays too much, and the brand because it shows their product does not hold its value.

As you can see, the determination of final-value is full of uncertainty and differing motivations. More than ever, beware the salesman here.

When making a large purchase, there are two options: save the money, or borrow the money. Deciding between the two can sometimes be a very clear and personal decision… other times there may be no choice at all. These are some situations where there are reduced choices:

In these cases, saving may not be a good option:

Saving the money may not be possible due to circumstance or timeline – when a sick parent suddenly needs to be cared for, and an additional bedroom is required. There isn’t time to put away extra money every month until a larger place can be paid for.

In the long run, borrowing may be less expensive than saving – renting an apartment over the many years could be more expensive than a mortgage as rent increases but fixed-rate mortgages stay stable.

The cost of a missed-opportunity while saving and waiting may be too high – when there’s a fantastically-paying new job, but it requires a car. The immediate increase in income due to the job could more than compensate for the expense of a car loan.

In these cases, getting a loan may not be a good option:

Borrowing is not available – especially with businesses needs, sometimes it’s just not possible to conventianally borrow money for that purpose

Credit rating problems – lenders either won’t participate due to credit rating, or the interest rate makes the loan unaffordable.

Can’t afford the item – even with the available down-payment, there’s not enough room in the budget to make the required payment each month.

Sometimes an immediate purchase cannot be made because borrowing and saving are both impossible. This is not a situation anyone wants to find themselves in during an emergency. When trying to be prepared, some of these exclusions can be avoided and others cannot. To be in the best possible situation during an unknown emergency, here are some general rules to follow:

Maintain good credit – some expenses are predictable and others are suprises, this can be critically important during an emergency

Have an current budget, updated with all expenses – to determine what is comfortably affordable

Keep to an emergency fund – to buy non-financalbe items, or use as a down-payment to achieve an affordable monthly payment

Save money every month – this allows room in the budget for the unexpected

Your individual circumstances should be taken into account when these decisions are made. If necessary, consult a financial advisor to help navigate these choices.

Lease agreements define a period of time where you will have use of something (a car). The items current value is determined, and the items value estimated at the end of the lease. The difference between

Borrowing money to pay for a car makes buying a car much easier. Your car loan may allow you to pay for a car over 5 years, but the car may last 10 years, 15 years or longer. Paying for the car quickly creates less risk for the lender, so you can expect a more favorable interest rate. At the end of the first 5 years the car is worth less than the amount you bought it for, but more than the zero you owe to the bank. While you were paying, you paid for more of the car than you used, and the remaining car is all yours! Leasing a car is another option. With a lease, you are trying to only pay for the amount of car that you’re going to use – to do this you’ll bargain to buy the car, and sell it back to the dealer at the end of the deal. Figuring out how much car gets used over a certain period of time involves determining the fair market-value of that car now, and at some projected point in the future given a certain amount of usage and maintenance. The difference between the value today, and the value at the end is what you will need to pay, with a fee for borrowing the money of course.